How and when to consider cross-securing - and when not to do it.

Whether you're investing in the rental market, or you're finally treating yourself to that holiday home you've had your eye on for years, you may have heard the term "cross-securing" touted as a potential solution.

If you already own (or are buying a property), cross-securing can be a great way to get a home loan for an investment property or summer home.

So what exactly is cross-securing and what are the main advantages and disadvantages?

Looking for a competitive home loan? Get a Rapid Quote.

How to Cross-secure Properties

How does it work?

Cross-securing properties is a way of using the equity in your home (the value of your home minus what you still owe on it) to fund the purchase of another.

Rather than put up cash to buy that second property, you can enter into a new home re-financing deal that takes equity out of your current house and uses it as the deposit for the second property.

In this type of refinancing, the bank or lender will combine the value of both properties, then subtract the equity in your current property to determine the total loan needed to cover both properties. Next, they will work out the LVR for the combined property loan and, as for any loan, assess whether you are able to service the total debt. If it all stacks up, the lender will take both properties as security on the new loan.

Of course, the more equity you have in your current home, the greater your chances are of getting a good deal on the new loan due to a favourable LVR.

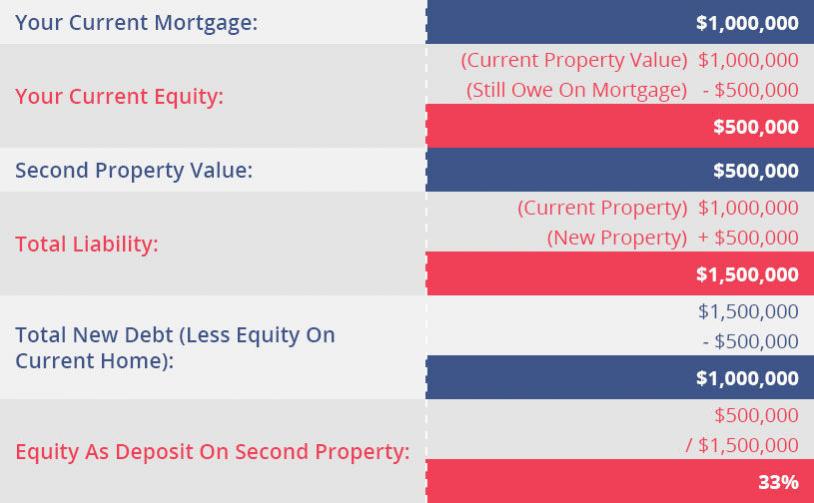

Example of cross-securing properties

Confused? Don't worry. Here's a simple example of cross-securing properties:

This means you’re putting down your equity on your current home as a 33% deposit, giving a loan to Value Ratio (LVR) of 66%.

Advantages

There are several advantages to using the cross-securing method to buy a new property.The main advantage however is that it helps you put down a substantial deposit.

While many lenders consider 5% an acceptable deposit, anything less than 20% may require Lender’s Mortgage Insurance (LMI) to be paid on top of your mortgage repayments. This the lender’s way of protecting themselves for taking on additional risk - they are exposing themselves to a 95% Loan to Value Ratio (LVR), meaning they’re fronting up the cash for nearly the whole property.

Rather than put up cash to buy that second property, you can enter into a new home re-financing deal that takes equity out of your current house and uses it as the deposit for the second property.

LMI is worth avoiding as it’s “dead money” - i.e. it doesn’t go towards paying off your actual mortgage. Paying it means less money in your pocket each month, and a lengthy ongoing expense that can add up to hundreds of thousands over the term of a mortgage.

However, cross-securing means you can use equity in your current home to get your Loan to Value Ratio (LVR) up to 20% and avoid paying LMI. In the above example, you've put down 33%, so no LMI payments are required.

Disadvantages

If you fail to make payments on either property’s mortgage, the bank can repossess both houses. So not only does the summer beach house get repossessed, so does your primary residence.

That said, this can be the case regardless of whether you have two separate mortgages for your two properties (held with a single lender), or a single cross-secured mortgage that covers both houses.

Is there any way to cross-secure without the risk of losing both properties?

Cross-securing must always be done with the same lender, so no.

However, you can instead opt to to have your two separate properties under split loans. In this scenario, you have two separate mortgages with two different lenders. This offers better protection as each property serves as security only for its own loan.

The ideal situation is to have enough cash for at least 20% deposit on your new home and split your mortgages up with separate lenders.

However, as most people don’t have a few hundred thousand in cash stuffed in a mattress, cross-securing can get you that second property - as long as you’re willing to accept the associated risk.

Still unsure of your options?

Call Rapid Finance. Our decades of expertise on cross-securing and property refinancing could find you the deal that suits you.

Call 1300 467 274 to discuss your situation today.