The formal options when you get into financial difficulty

Moving on from financial trouble

This information is general information only. If you are in serious financial trouble, including personal insolvency, seek professional advice.

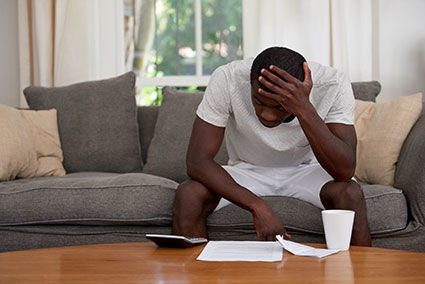

When you get into serious financial trouble, there are some options you can consider in order to get your life back on track. First, there are informal options, such as negotiating a payment plan with your creditors (the people to whom you owe money) or alternative arrangements.

However, when your debt becomes unmanageable, and you are 'insolvent', which means you are unable to pay your debts as and when they fall due, there are some formal arrangements you can make. These are agreements entered into between you and your creditors, which are covered in legislation outlined in the Bankruptcy Act 1966, and include full Bankruptcy and a Part IX Debt Agreement.

The consequences of these agreements are serious: getting finance while these arrangements are in place is generally impossible, and your credit history will be affected for many years afterwards. But having a bad credit history is not the end of the world – there is life after bankruptcy! Not

At Rapid Finance, we specialise in bad credit personal loans and bad credit car finance, even if you have been previously been declared bankrupt. Talk to a bad credit loan expert today on 1300 467 274 to see how we may be able to help you.

What is Full Bankruptcy?

Bankruptcy is a legal status for individuals who are insolvent. This means that the law recognises that you cannot meet your financial obligations to your creditors. You can become voluntarily bankrupt by lodging a 'debtor’s petition', or a creditor may take court action to have you declared bankrupt.

If you are declared bankrupt, a trustee will be appointed who will attempt to recover some of the debt owing to your creditors, which may include selling your assets and investigating your financial affairs. The period of bankruptcy lasts three years, and during this time creditors are not allowed to continue to demand payment. Once the bankruptcy ends, you are generally not required to pay any more outstanding debts.

Are your financial mistakes in the past once bankruptcy is over? Not exactly. Bankruptcy is listed on your credit history, and credit reporting agencies can keep a record of your bankruptcy for up to five years, sometimes longer. But it’s not all bad news. At Rapid Finance, we understand that a previous bankruptcy should be left in the past. Find out more about applying for bad credit loans when declared bankrupt.

What is a Part IX Debt Agreement?

A debt agreement, also known as a Part IX Debt Agreement, is an alternative to full bankruptcy. However, it is still considered an 'act of bankruptcy'. A debt agreement is a binding agreement where your creditors have agreed to accept a sum of money and in turn release you from some of your debts.

You, the debtor, can propose a debt agreement, which will be received by your creditors. If they accept the terms of the agreement, your creditors have agreed to receive an amount of money that you can afford to pay back to them. Generally, interest and fees are frozen whilst you pay back the agreed amount.

The agreement ends when all your agreed obligations and payments have been met. As a debt agreement is still an act of bankruptcy, it is noted on your credit history for a number of years. This can make getting finance difficult, but not impossible - see car loans with a part ix debt agreement.

It is not a good idea to apply for personal finance if you are either bankrupt or in a debt agreement.

What is the difference?

A key difference is that a Part IX Debt Agreement is initiated by you, by proposing a formal arrangement to your creditors. With full bankruptcy – although you can voluntarily elect for bankruptcy – your creditors can force you into becoming bankrupt.

There are also differences in making payments to secured and unsecured creditors, and your ability to retain your assets. The following table summarises the key differences between bankruptcy and a debt agreement.

| Bankruptcy | Debt agreement | |

|---|---|---|

|

Are payments from my income required? |

Only if your income exceeds certain amount. |

Generally yes. |

|

Will my assets be sold? |

Yes, however some assets will be protected including household items and some tools and vehicles. |

Depends on terms outlined in agreement. |

|

Can I get new assets? |

Generally no. |

Yes. |

|

What happens to my unsecured debts? |

Creditors may receive some payments from the sale of your assets. |

Creditors receive payments as outlined in debt agreement. |

|

What happens to my secured debts? |

No change to the rights of secured creditors. |

No change to the rights of secured creditors. |

Source: Australian Financial Security Authority

Get professional advice

Bankruptcy and debt agreements are serious issues and, no matter how well you handle it, you will feel financial and emotional pain. But, if you handle it properly and professionally, you can minimise that pain and move on with your life.

If you get it wrong, the consequences could haunt you for a long time. Professional advice is essential if you want to minimise your difficulties.

Rapid Finance can't give you that professional advice, but we do urge anyone who is facing the sort of financial problems that could lead to bankruptcy or a Part IX agreement to talk to someone who specialises in these matters.

Can I get finance?

It is not a good idea to apply for vehicle finance if you are either bankrupt or in a debt agreement. During this time, you should be focusing on paying off outstanding debts and meeting your existing obligations.

Once you have been discharged from bankruptcy or your debt agreement, then you can apply for finance. The record of your financial troubles can stay on your credit history for over 5 years, which may lock you out of some finance options – but not all.

Finance brokers like Rapid Finance specialise in working with people with previous financial troubles to obtain finance. If you have a bad credit history and have been knocked back before, then we may be able to assist you get approval on personal loans with bad credit that might work for you.

Call us on 1300 467 274 to see if we can help you.

This information is general information only and is not intended as advice. If you are in serious financial trouble, including personal insolvency, please visit the Australian Financial Security Authority’s page on seeking help.