Is There Any Way to Get Them Removed Quickly?

Your credit history is a comprehensive document that covers your history where credit facilities like loans, credit cards, and mortgages are concerned.

And while the rules have recently changed to include a larger amount of positive information (such as paying your bills on time and in full), the information generally relates to poor financial conduct - such as missed payments and bankruptcies.

So, how long does this information stay on your credit history? And are there different terms for defaults compared with other credit infringements?

Looking for a competitive car loan? Get a Free Finance Assessment.

What would I receive credit defaults for?

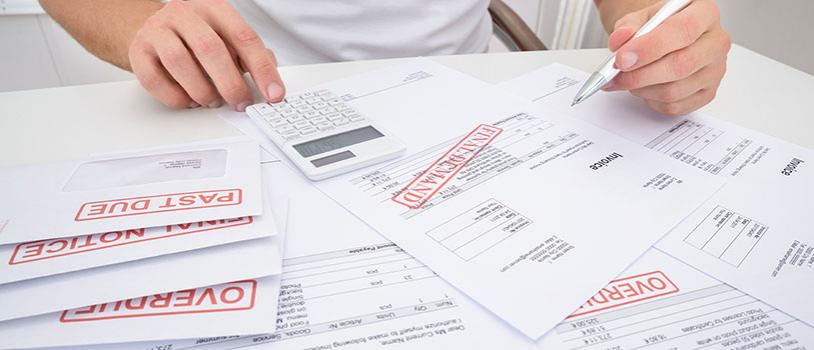

The most common example of a black mark on your credit history is a creditor listing a default against you.

Credit defaults refer specifically to a mark on your credit history for an unpaid bill or other debt. The most common types of defaults that may be listed on a credit history are for utility bills, telco bills, loan repayments, credit card payments and mortgage repayments.

Failure or refusal to pay these types of bills may result in your bank, lender, telco, or utilities provider listing a default against you. However, to do so, they must prove they have made reasonable efforts to contact you and have given you ample opportunity to settle the payment(s).

How long do defaults stay on my history?

In general, defaults stay on your credit history for five years. It’s important to note that once you have paid a default, it will remain on your history for the full five years period, though it will be listed as “paid”.

Other more serious types of more credit infringement may stay on your history for up to seven years, including certain types of bankruptcy.

That five year rule applies to most minor credit infringements. The two notable exceptions are court writs, which stay on your history for four years and “clearouts”, which stay for seven years. A clearout is a more serious credit infringement where the individual owes a debt to a credit provider but has left, or appears to have left, their last address without paying meeting the debt. Without providing the credit provider with their new address.

Other more serious types of credit infringements may stay on your history for up to seven years, including certain types of bankruptcy. Read more about whether you can get a loan if declared bankrupt.

Can I get these infringements off my credit history?

Possibly. If you can prove the default or infringement was listed in error, or that the creditor did not make reasonable efforts to contact you, they may be forced to remove it.

Credit repair agencies specialise in investigating matters like this. However, unless the creditor has shown negligence, the default will remain on your history for the full term.

Will defaults on my credit history stop me getting finance in the future?

Maybe, but not necessarily. It depends on whether the default has been paid and on your financial and personal circumstances.

With over two decades of experience, Rapid Finance has built a reputation of matching our clients with the right lender. No matter your situation, we can help you find a suitable loan.

If you are interested in a new car but worried about credit, you can speak to one of our credit experts or view our car loan options and apply online.